目录

一 线性回归

2.代码

% Perform the parametric linear regression

clear, close all

clc

%% load Advertising data:

% Sales (in thousands of units) for a particular product as a function of advertising budgets

% (in thousands of dollars) for TV, radio, and newspaper media.

[num,txt,raw]=xlsread('Advertising.csv');

Sales=num(:,5);

TV=num(:,2);

Radio=num(:,3);

Newspaper=num(:,4);

%% Perform univariate linear regression on TV advertising budget

%%% Regress "Sales" on "TV"

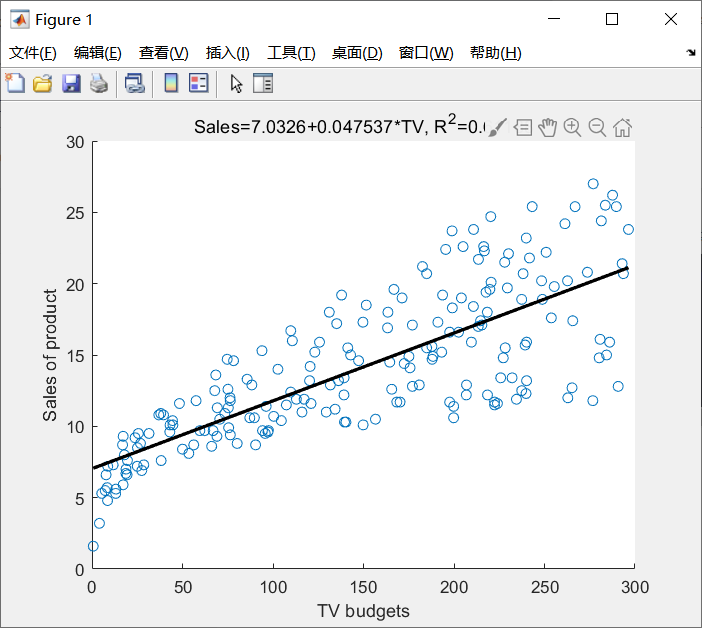

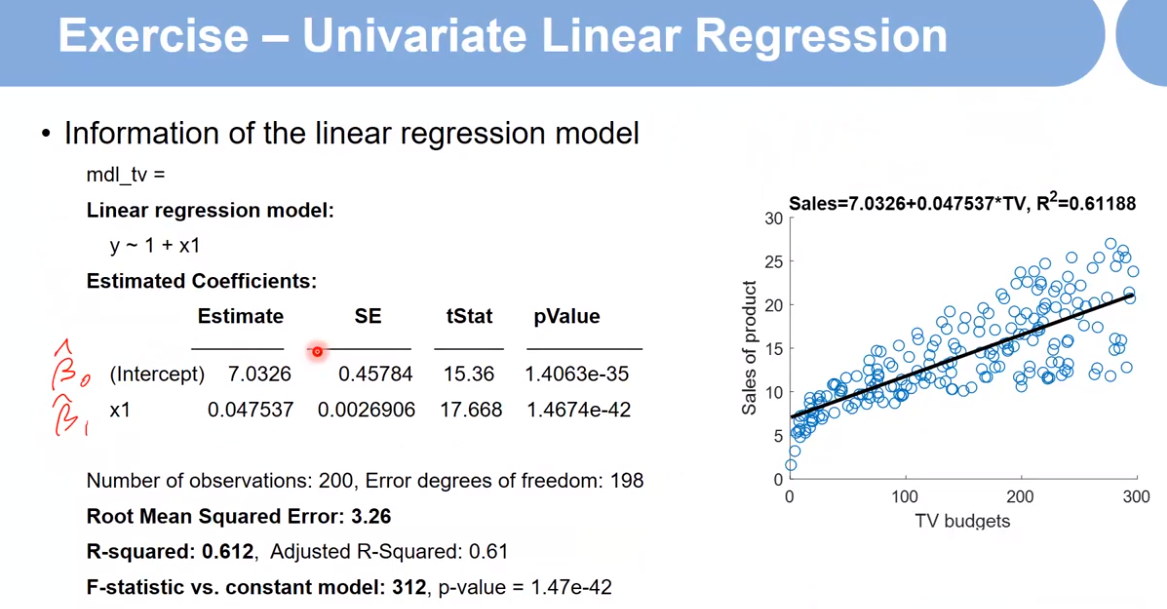

mdl_tv = fitlm(TV,Sales)

% mdl_tv.Coefficients

% mdl_tv.RMSE

% mdl_tv.Rsquared.Ordinary

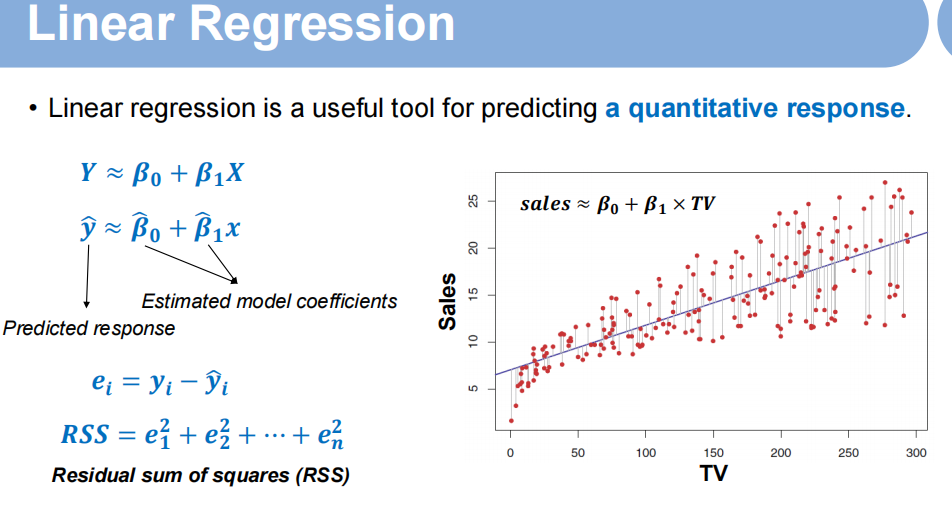

figure,

scatter(TV,Sales), hold on

plot([min(TV), max(TV)],[predict(mdl_tv,min(TV)), predict(mdl_tv,max(TV))],'k-','linewidth',2)

xlabel('TV budgets'), ylabel('Sales of product')

title(['Sales=' num2str(mdl_tv.Coefficients.Estimate(1)) '+' ...

num2str(mdl_tv.Coefficients.Estimate(2)) '*TV',...

', R^2=' num2str(mdl_tv.Rsquared.Ordinary)])

%% Perform multiple linear regression on all advertising budgets

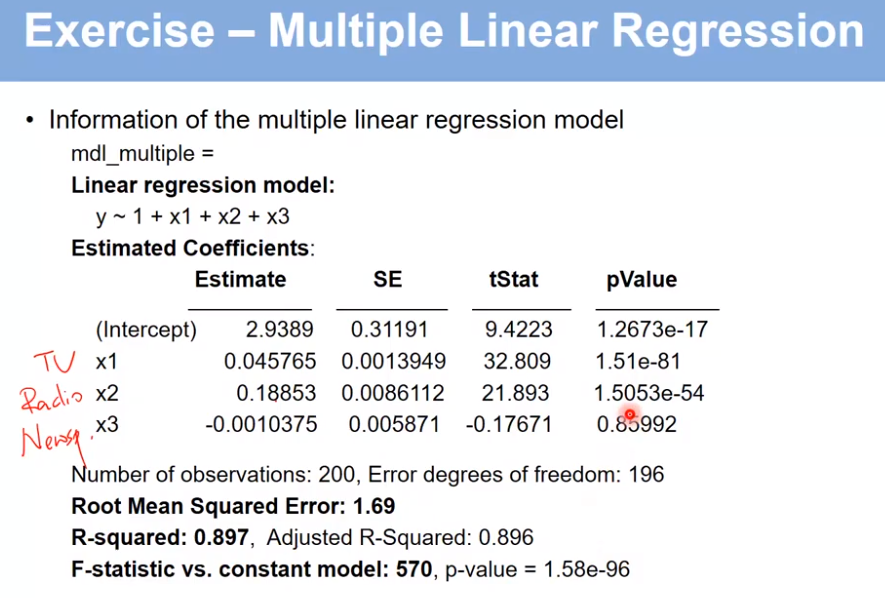

mdl_multiple = fitlm([TV,Radio,Newspaper],Sales)

%%% check the correlations between different types of budgets

[rho,p]=corr([TV,Radio,Newspaper]);

结果如下:

scatter(TV,Sales) 画出散点图

mdl_tv = fitlm(TV,Sales) 表示单因子线性回归分析

plot([min(TV), max(TV)],[predict(mdl_tv,min(TV)), predict(mdl_tv,max(TV))],’k-‘,’linewidth’,2)

[min(TV), max(TV)] 给出图形的范围

predict函数表示给定一个模型,还有一个输入参数,能够得出模型的输出参数

mdl_multiple = fitlm([TV,Radio,Newspaper],Sales) 多因子回归分析

[rho,p]=corr([TV,Radio,Newspaper]) 衡量三个系数之间的相关性。

rho得出任意两个系数之间的相关系数,是一个系数矩阵,越大则相关性越强;p得出相关系数的显著性,是一个矩阵,越小则越显著

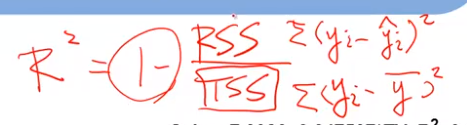

R^2:代表拟合效果,越接近1越好。 F:越大越好 pValue:代表显著性,越小越好

二 非线性回归

1.理论

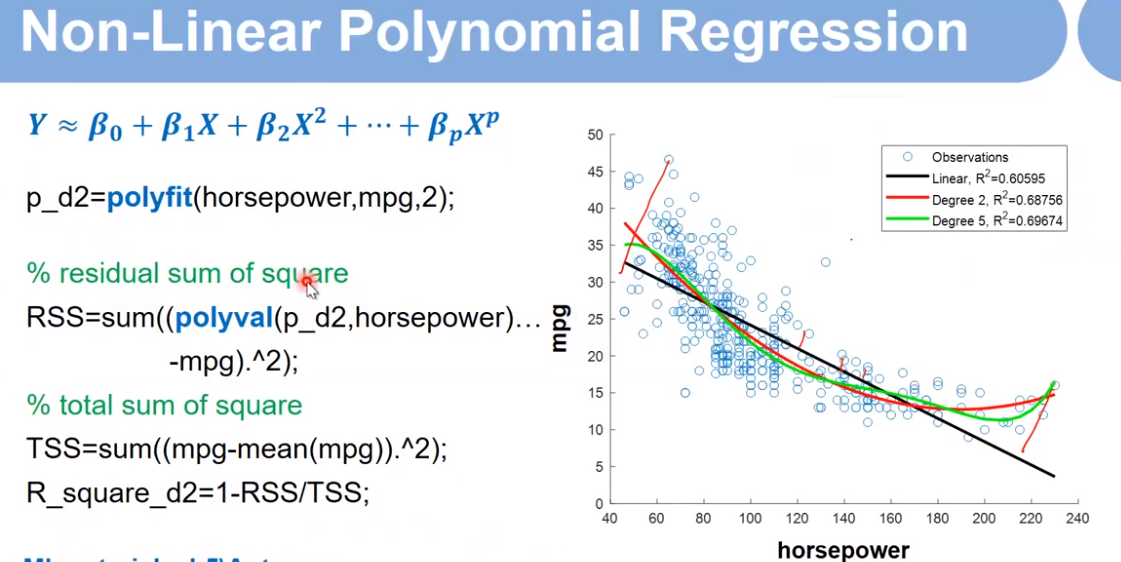

% Perform the parametric polynomial regression

clear, close all

%% load Auto data:

[num,txt,raw]=xlsread('Auto.csv');

mpg=num(:,1); % gas mileage in miles per gallon

horsepower=num(:,4);

excludeind=find(isnan(horsepower)); % identify the indices with missing horsepower data

mpg(excludeind,:)=[]; % remove the observations with missing horsepower data

horsepower(excludeind,:)=[]; % remove the observations with missing horsepower data

%% perform polynomial regression

p_d1=polyfit(horsepower,mpg,1); % linear

RSS=sum((polyval(p_d1,horsepower)-mpg).^2); % residual sum of square

TSS=sum((mpg-mean(mpg)).^2); % total sum of square

R_square_d1=1-RSS/TSS;

p_d2=polyfit(horsepower,mpg,2); % Degree 2

RSS=sum((polyval(p_d2,horsepower)-mpg).^2); % residual sum of square

TSS=sum((mpg-mean(mpg)).^2); % total sum of square

R_square_d2=1-RSS/TSS;

p_d5=polyfit(horsepower,mpg,5); % Degree 5

RSS=sum((polyval(p_d5,horsepower)-mpg).^2); % residual sum of square

TSS=sum((mpg-mean(mpg)).^2); % total sum of square

R_square_d5=1-RSS/TSS;

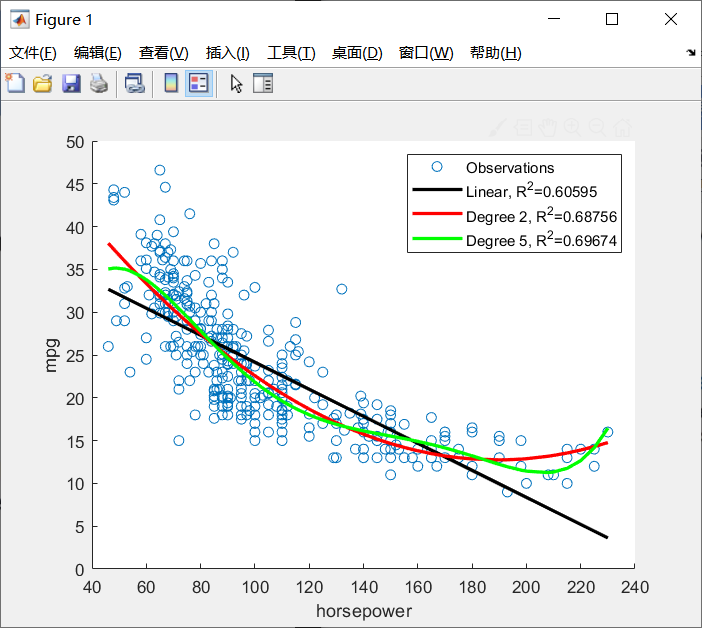

figure,

scatter(horsepower,mpg), hold on

x=sort(horsepower);

plot(x,polyval(p_d1,x),'k-','linewidth',2)

plot(x,polyval(p_d2,x),'r-','linewidth',2)

plot(x,polyval(p_d5,x),'g-','linewidth',2)

xlabel('horsepower'), ylabel('mpg')

legend('Observations',...

['Linear, R^2=' num2str(R_square_d1)],...

['Degree 2, R^2=' num2str(R_square_d2)],...

['Degree 5, R^2=' num2str(R_square_d5)])

p_d2=polyfit(horsepower,mpg,2);

horsepower:输入,x轴 mpg:y轴 2:最高只有2次项

polyval(p_d2,horsepower) 预测函数

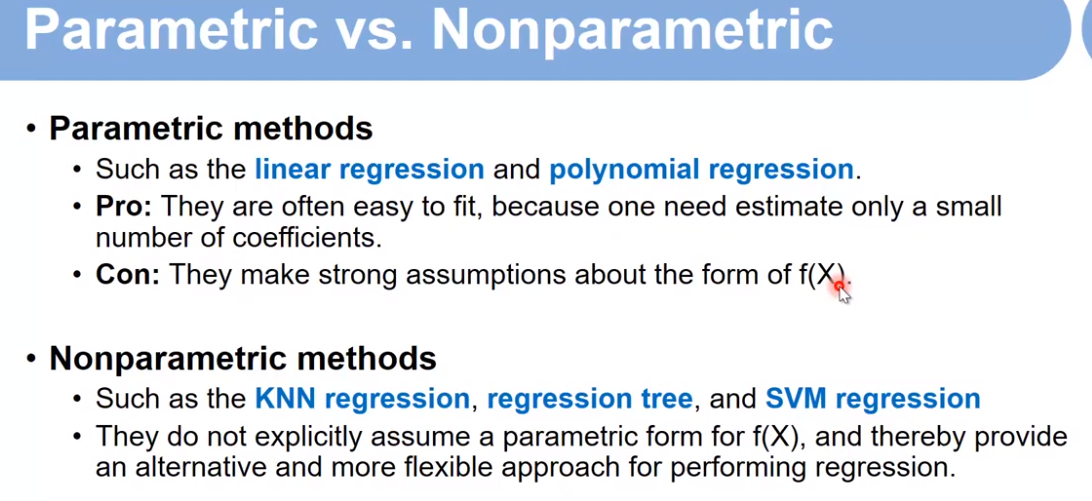

三 Nonparametric methods

3.1理论

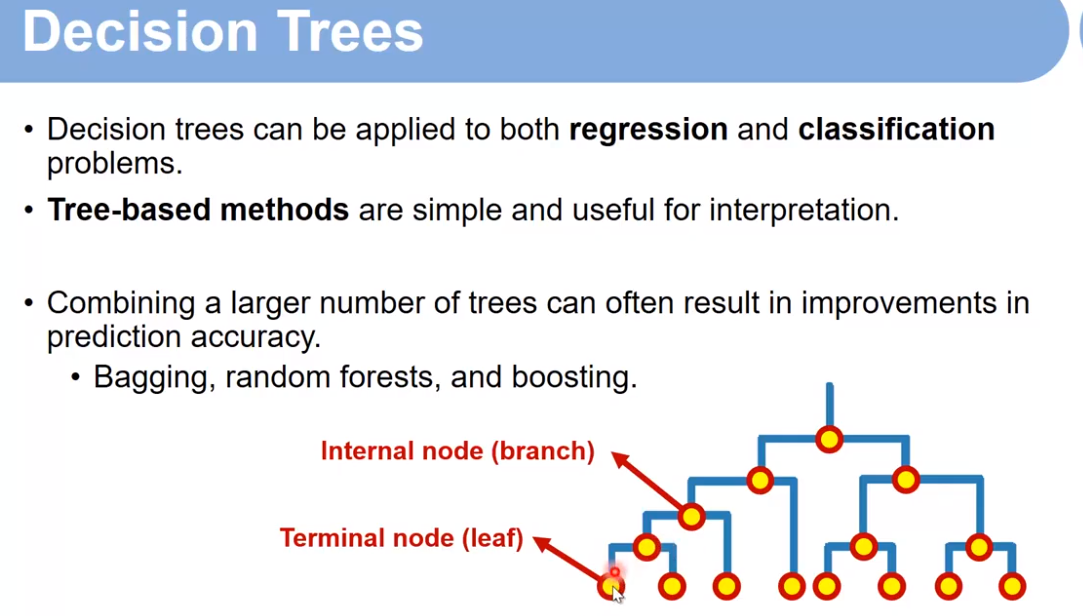

3.2Decision Trees

3.3代码

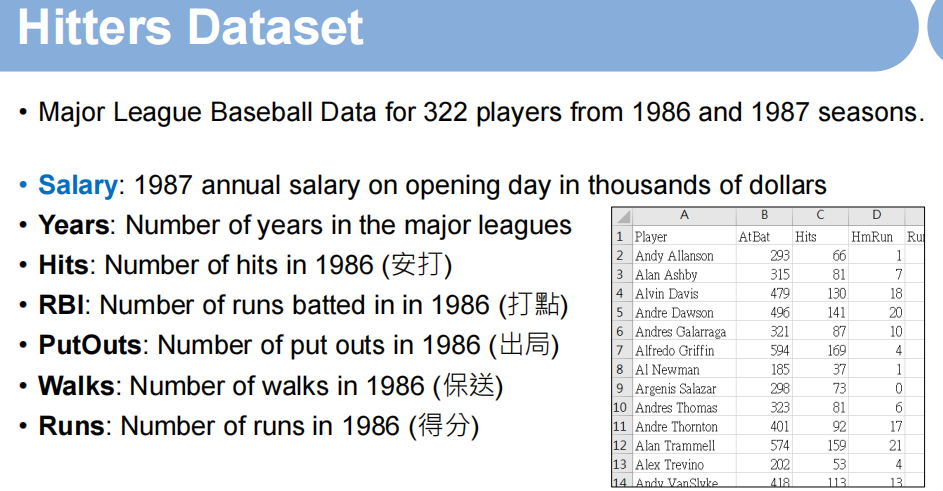

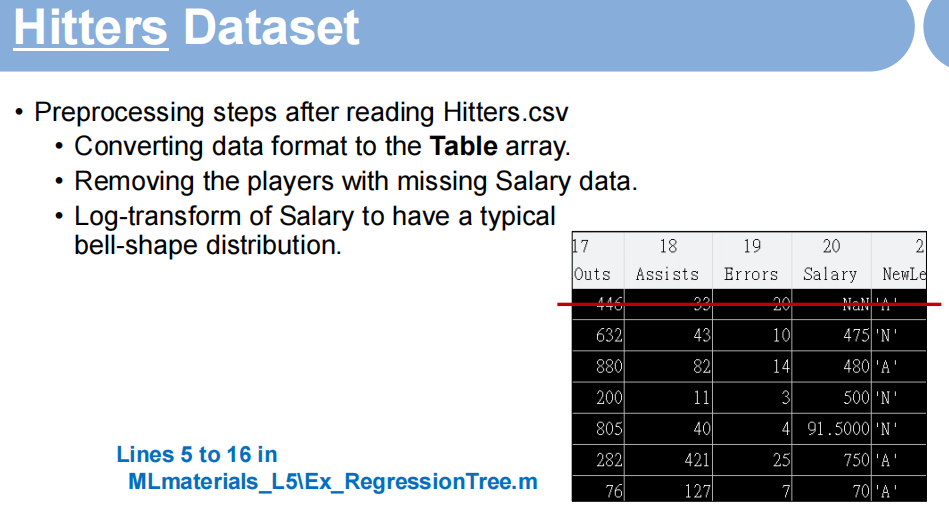

准备数据集,数据预处理

将数据转换为table类型,并且第一行的数据不转换:

data=cell2table(raw(2:end,:))

定义变量名:

for i=1:size(data,2)

data.Properties.VariableNames{i}=raw{1,i}; % assign the VariableNames

end

去除无用数据:

excludeind=find(isnan(data.Salary)); % identify the indices with missing Salary data

data(excludeind,:)=[]; % remove the players with missing Salary data

取log函数(其实是ln,自然对数为底)使数据更平滑:

data.Salary=log(data.Salary); % log-transform to have a typical bell-shape distribution

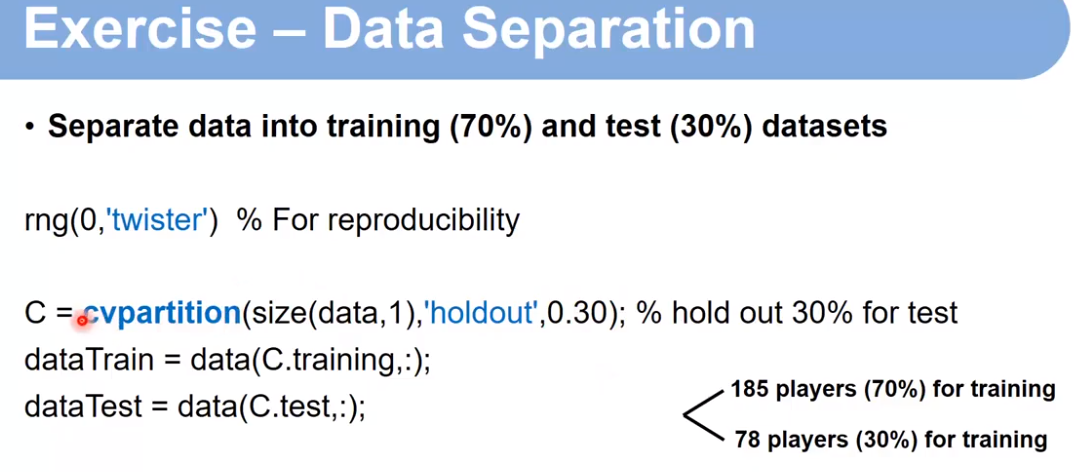

数据集分解:

建立模型

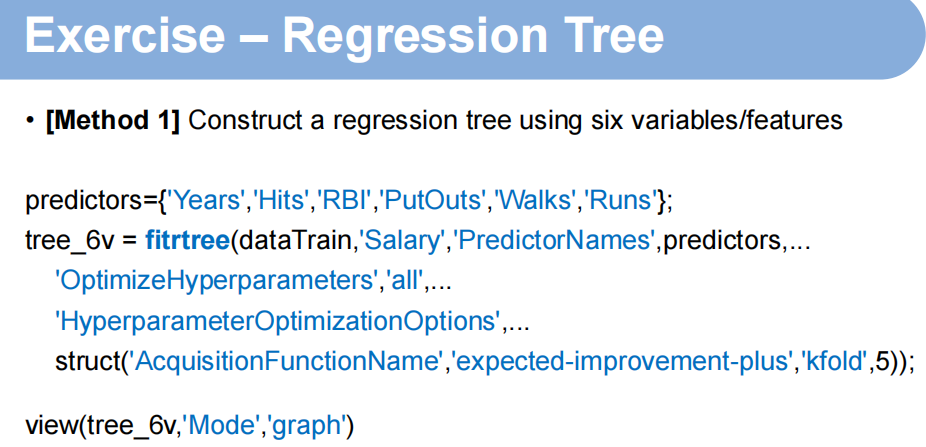

第一步:

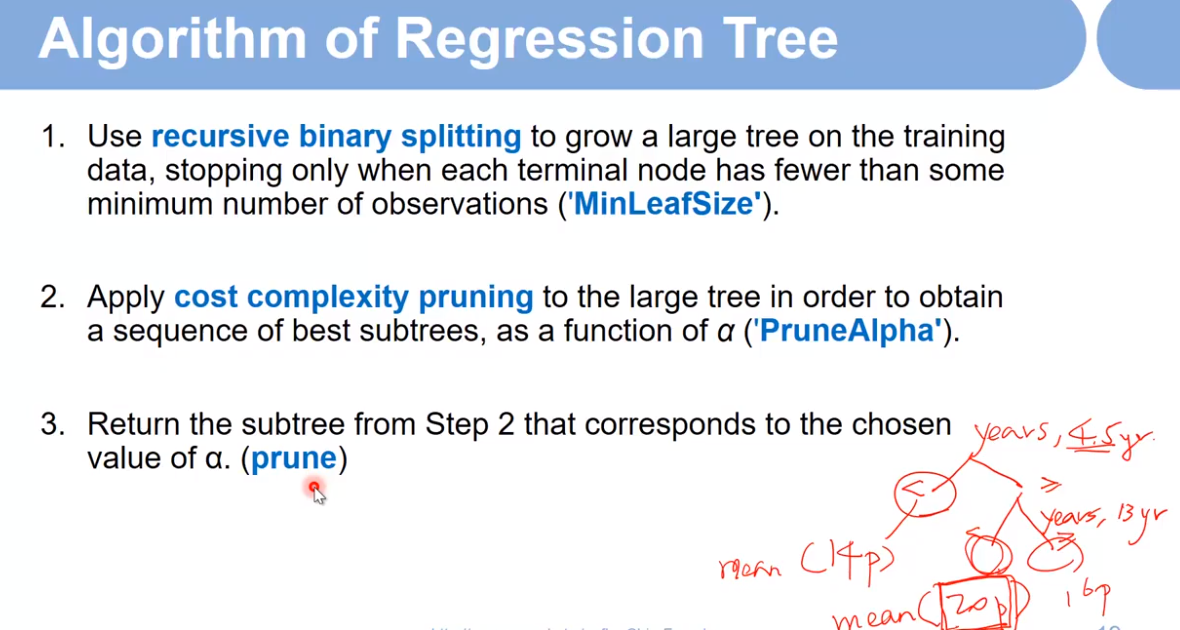

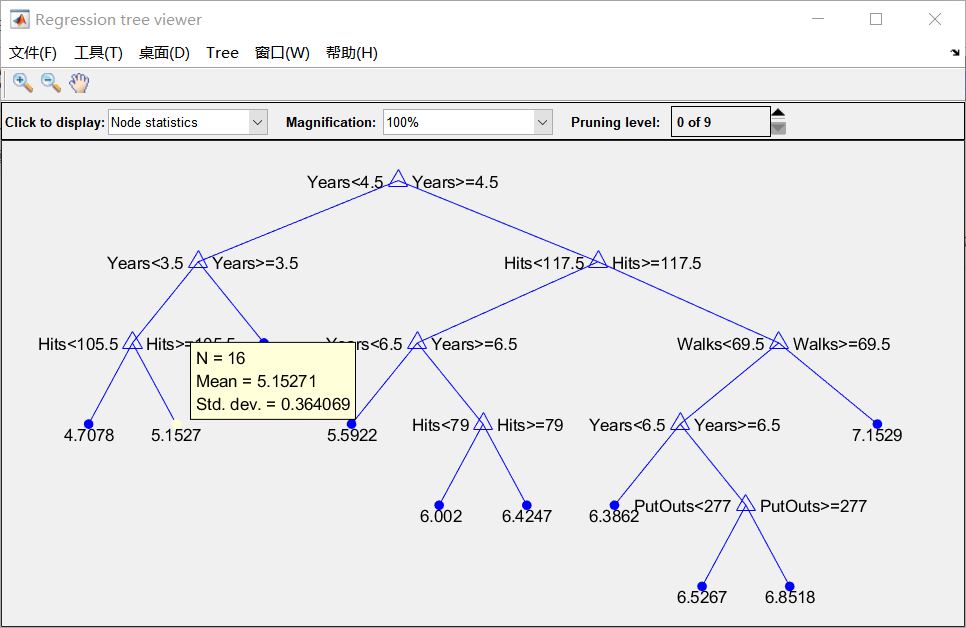

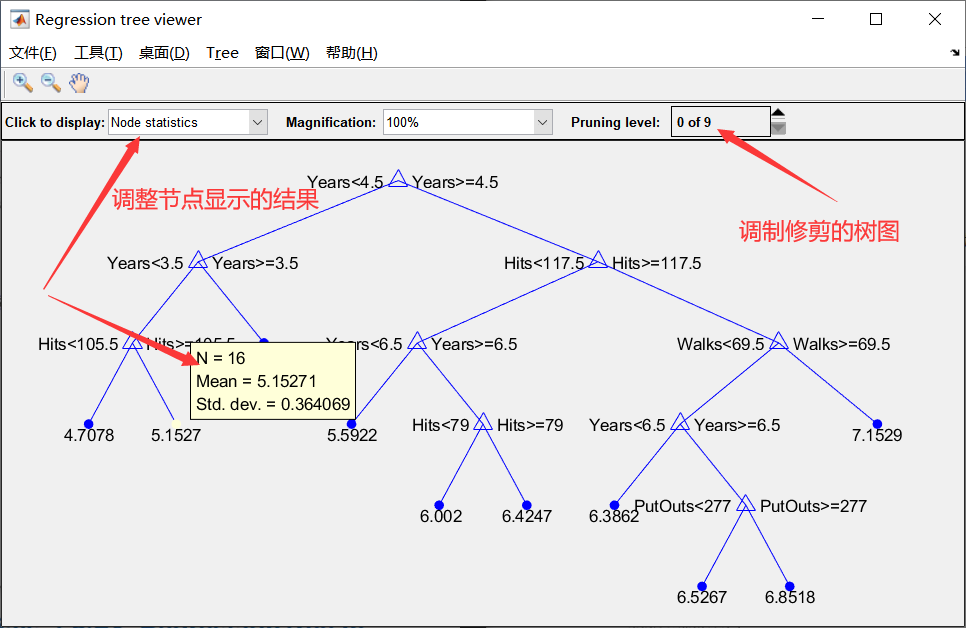

选定六个指标;选定salary作为衡量标准,交叉验证,分为5折;view函数为画出树图,如下:

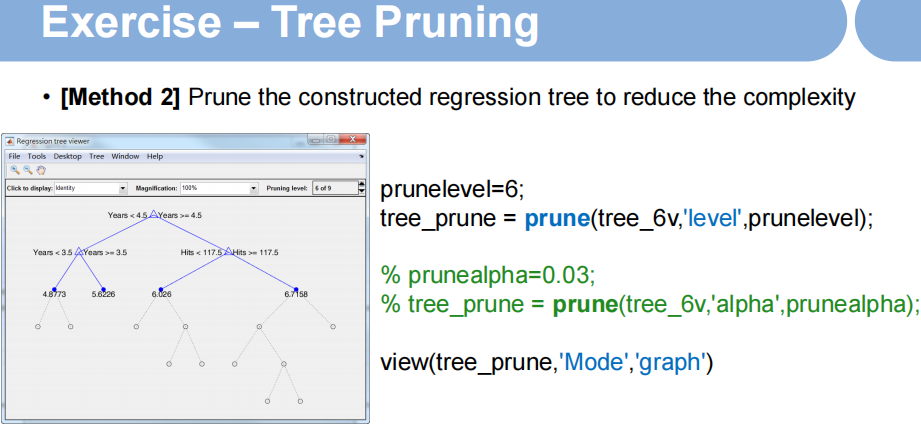

第二步:修建树图

改prunelevel或者prunealpha

也可以直接在图片上面修改:

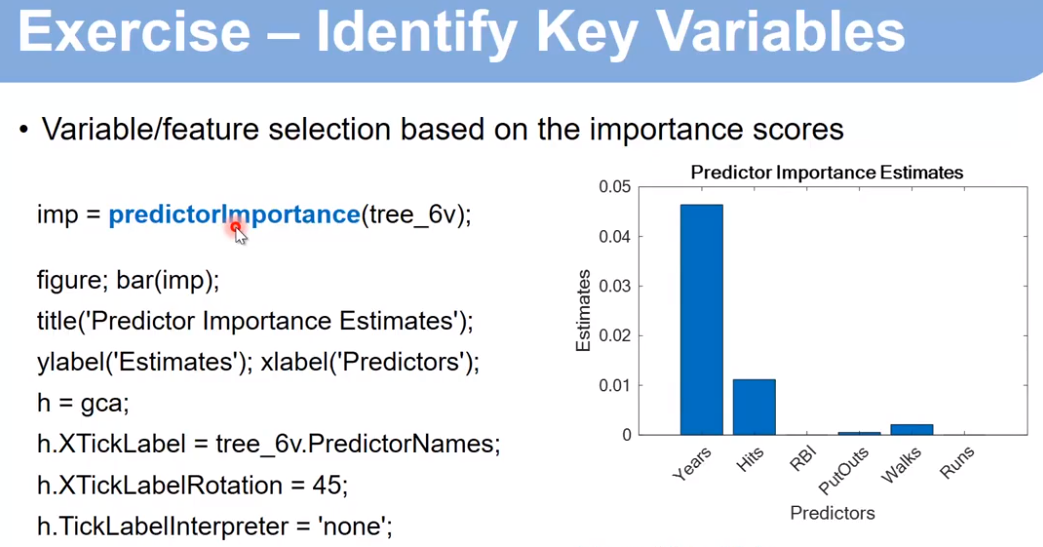

查看参数的重要程度:

imp = predictorImportance(tree_6v);

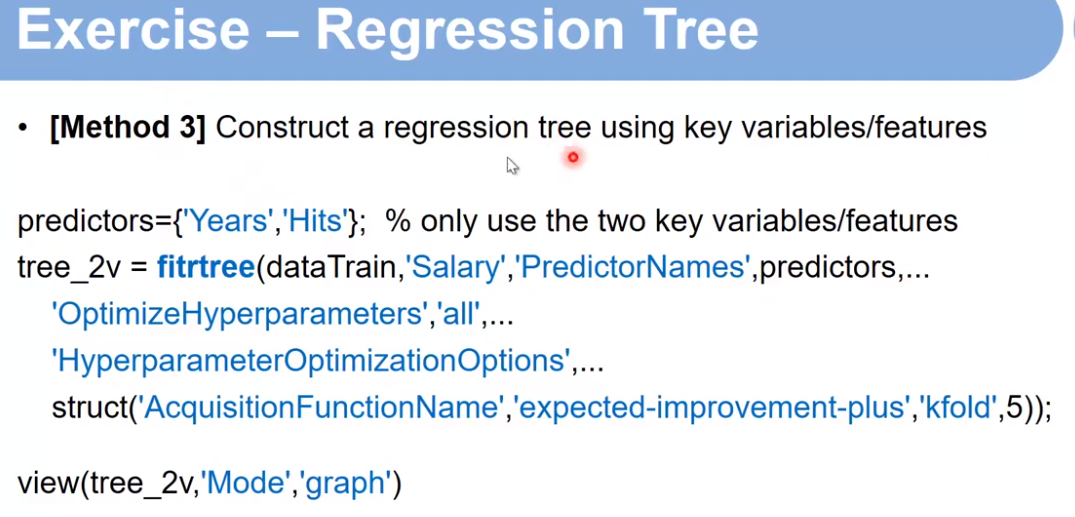

第三步:只用两个参数运行模型

完整代码:

% Perform the regression tree using "fitrtree" function

clear, close all

%% load Hitters data: Major League Baseball Data from the 1986 and 1987 seasons.

[num,txt,raw]=xlsread('Hitters.csv');

% construct Table array

data=cell2table(raw(2:end,:));

for i=1:size(data,2)

data.Properties.VariableNames{i}=raw{1,i}; % assign the VariableNames

end

excludeind=find(isnan(data.Salary)); % identify the indices with missing Salary data

data(excludeind,:)=[]; % remove the players with missing Salary data

data.Salary=log(data.Salary); % log-transform to have a typical bell-shape distribution

%% Separate data into training (70%) and test (30%) datasets

rng(0,'twister') % For reproducibility,可删除这一行代码,只是为了保证随机数是一样的

C = cvpartition(size(data,1),'holdout',0.30); % randomly hold out 30% of subjects for test

dataTrain = data(C.training,:);

dataTest = data(C.test,:);

%% [Method 1] Construct a regression tree using six variables/features

% Construct a regression tree using the training dataset

predictors={'Years','Hits','RBI','PutOuts','Walks','Runs'};

tree_6v = fitrtree(dataTrain,'Salary','PredictorNames',predictors,...

'OptimizeHyperparameters','all',...

'HyperparameterOptimizationOptions',...

struct('AcquisitionFunctionName','expected-improvement-plus','kfold',5));

view(tree_6v,'Mode','graph')

% Test the tree model on the test dataset

Salary_predict=predict(tree_6v,dataTest);

MSE=loss(tree_6v,dataTest); % mean squared error, MSE=mean((Salary_predict-dataTest.Salary).^2);

RSS=sum((Salary_predict-dataTest.Salary).^2); % residual sum of square

TSS=sum((dataTest.Salary-mean(dataTest.Salary)).^2); % total sum of square

R_square=1-RSS/TSS;

figure,plot(1:size(dataTest,1),dataTest.Salary,'r.-',1:1:size(dataTest,1),Salary_predict,'b.-')

title(['[Method 1] MSE = ' num2str(MSE) ', R^2 = ' num2str(R_square)])

legend('True salaries','Predicted salaries')

xlabel('Players'),ylabel('Salaries')

%% [Method 2] Construct a regression tree using six variables/features with pruning

prunelevel=6;

tree_prune = prune(tree_6v,'level',prunelevel);

% prunealpha=0.03;

% tree_prune = prune(tree_6v,'alpha',prunealpha);

view(tree_prune,'Mode','graph')

% Test the tree model on the test dataset

Salary_predict=predict(tree_prune,dataTest);

MSE=loss(tree_prune,dataTest); % mean squared error, MSE=mean((Salary_predict-dataTest.Salary).^2);

RSS=sum((Salary_predict-dataTest.Salary).^2); % residual sum of square

TSS=sum((dataTest.Salary-mean(dataTest.Salary)).^2); % total sum of square

R_square=1-RSS/TSS;

figure,plot(1:size(dataTest,1),dataTest.Salary,'r.-',1:1:size(dataTest,1),Salary_predict,'b.-')

title(['[Method 2] MSE = ' num2str(MSE) ', R^2 = ' num2str(R_square)])

legend('True salaries','Predicted salaries')

xlabel('Players'),ylabel('Salaries')

%% Variable/Feature selection based on the importance scores

imp = predictorImportance(tree_6v);

figure;

bar(imp);

title('Predictor Importance Estimates');

ylabel('Estimates');

xlabel('Predictors');

h = gca;

h.XTickLabel = tree_6v.PredictorNames;

h.XTickLabelRotation = 45;

h.TickLabelInterpreter = 'none';

%% [Method 3] Construct a regression tree using key variables/features

% Construct a regression tree using the training dataset

predictors={'Years','Hits'}; % only use the two key variables/features

tree_2v = fitrtree(dataTrain,'Salary','PredictorNames',predictors,...

'OptimizeHyperparameters','all',...

'HyperparameterOptimizationOptions',...

struct('AcquisitionFunctionName','expected-improvement-plus','kfold',5));

view(tree_2v,'Mode','graph')

% Test the tree model on the test dataset

Salary_predict=predict(tree_2v,dataTest);

MSE=loss(tree_2v,dataTest); % mean squared error, MSE=mean((Salary_predict-dataTest.Salary).^2);

RSS=sum((Salary_predict-dataTest.Salary).^2); % residual sum of square

TSS=sum((dataTest.Salary-mean(dataTest.Salary)).^2); % total sum of square

R_square=1-RSS/TSS;

figure,plot(1:size(dataTest,1),dataTest.Salary,'r.-',1:1:size(dataTest,1),Salary_predict,'b.-')

title(['[Method 3] MSE = ' num2str(MSE) ', R^2 = ' num2str(R_square)])

legend('True salaries','Predicted salaries')

xlabel('Players'),ylabel('Salaries')

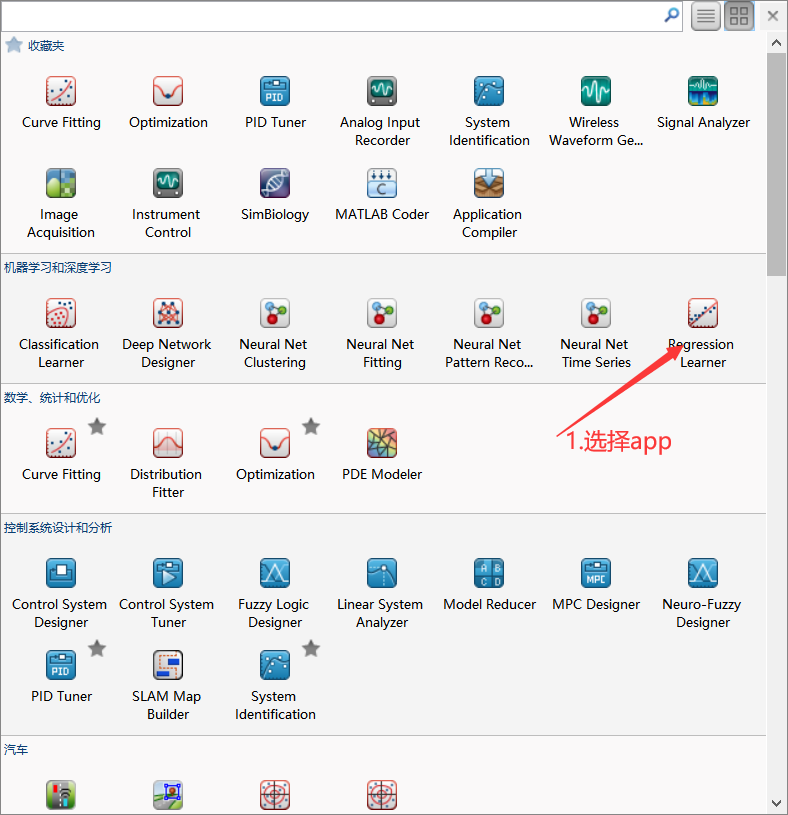

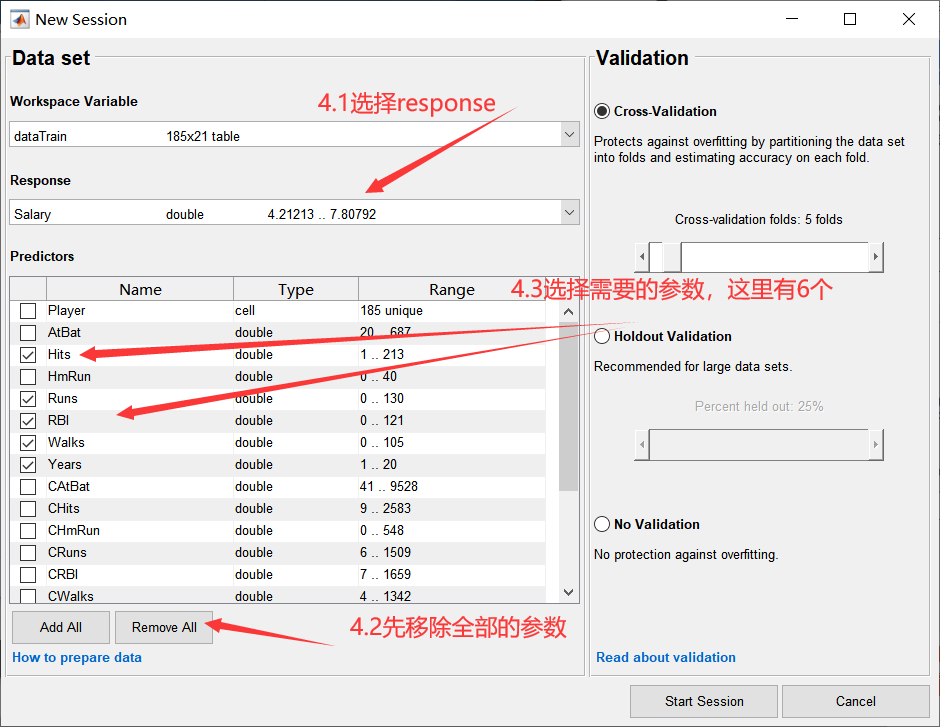

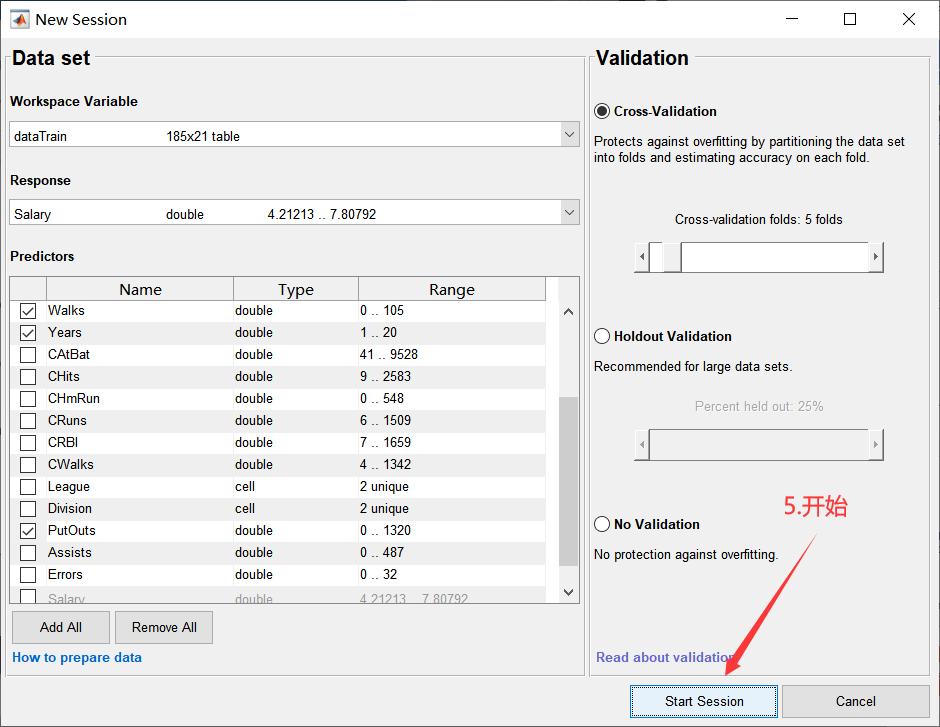

四 APP使用

比较适合熟悉基本的模型,但是因为是一个包装好的模型,所以不能调节具体的参数,如果真正的要运行一个模型并且查看和调节各种参数,还是需要自己去写代码来运行。

下面是使用APP的具体方法!

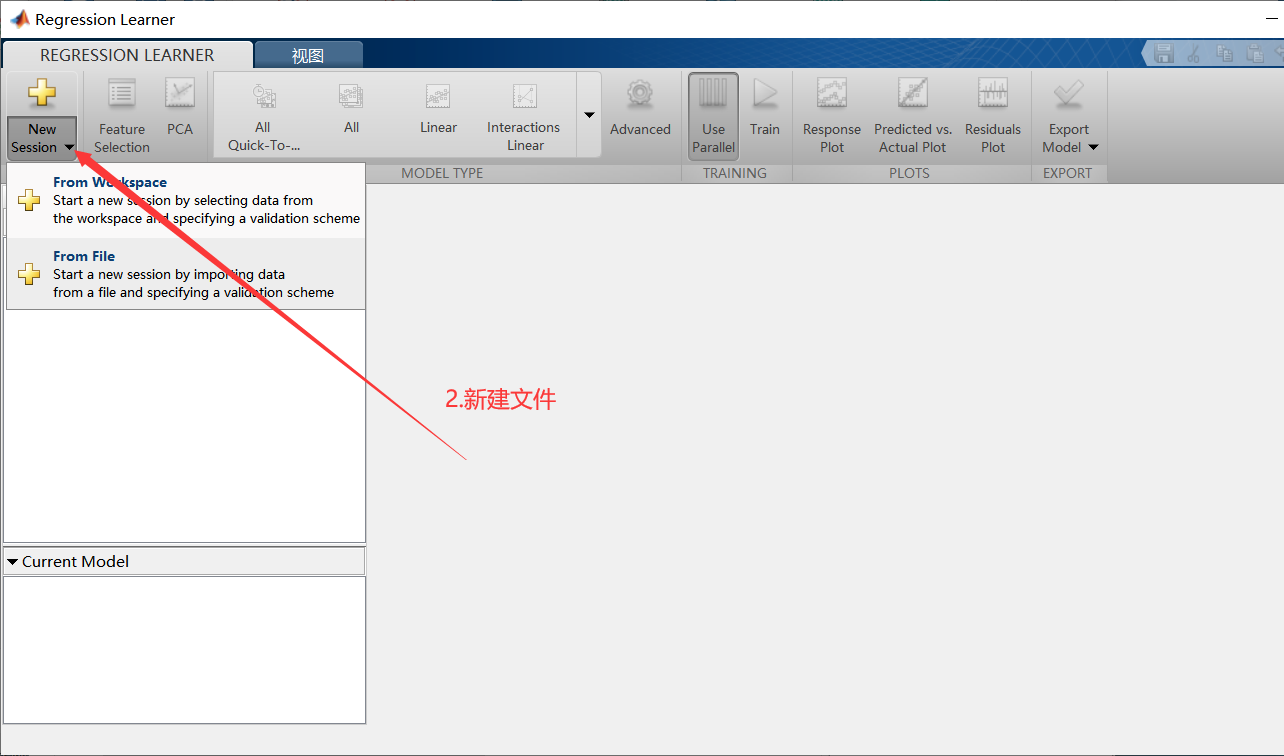

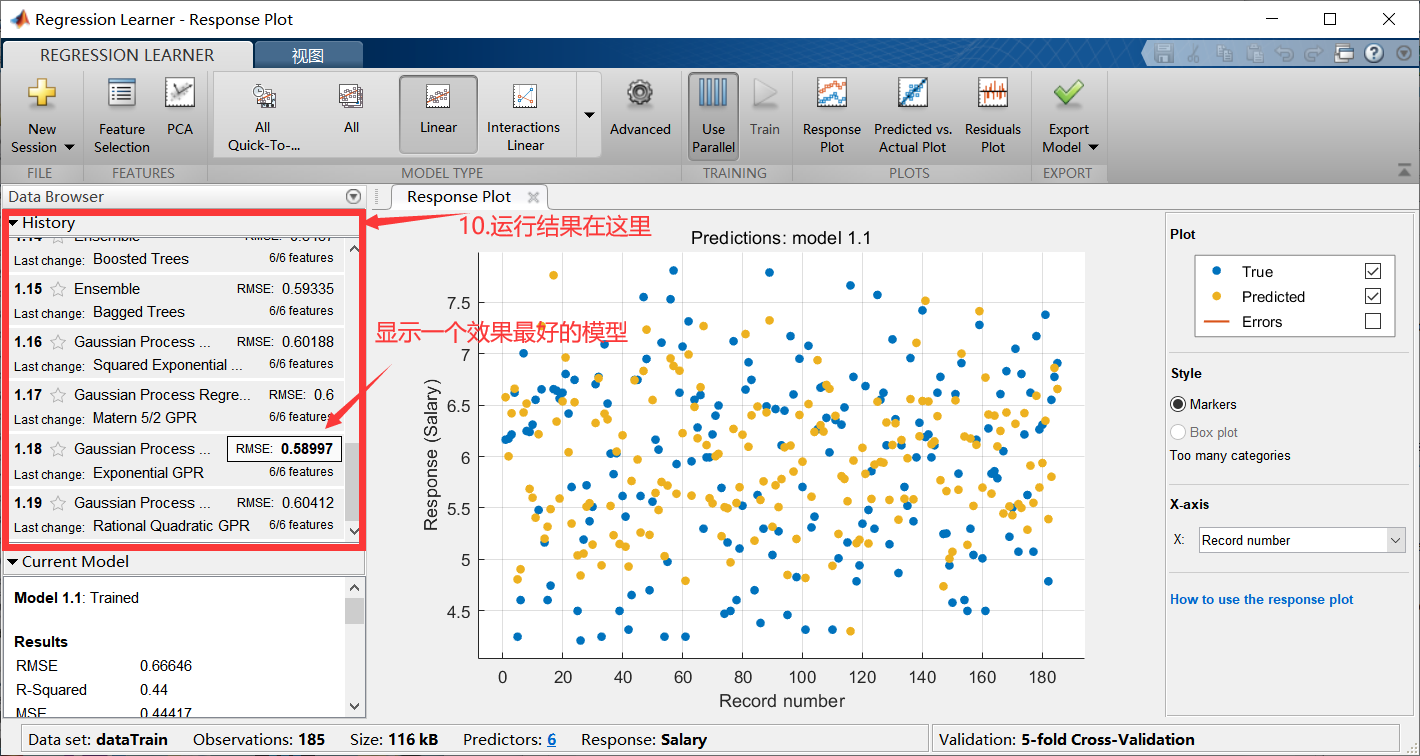

开始后会回到新建界面,如下:

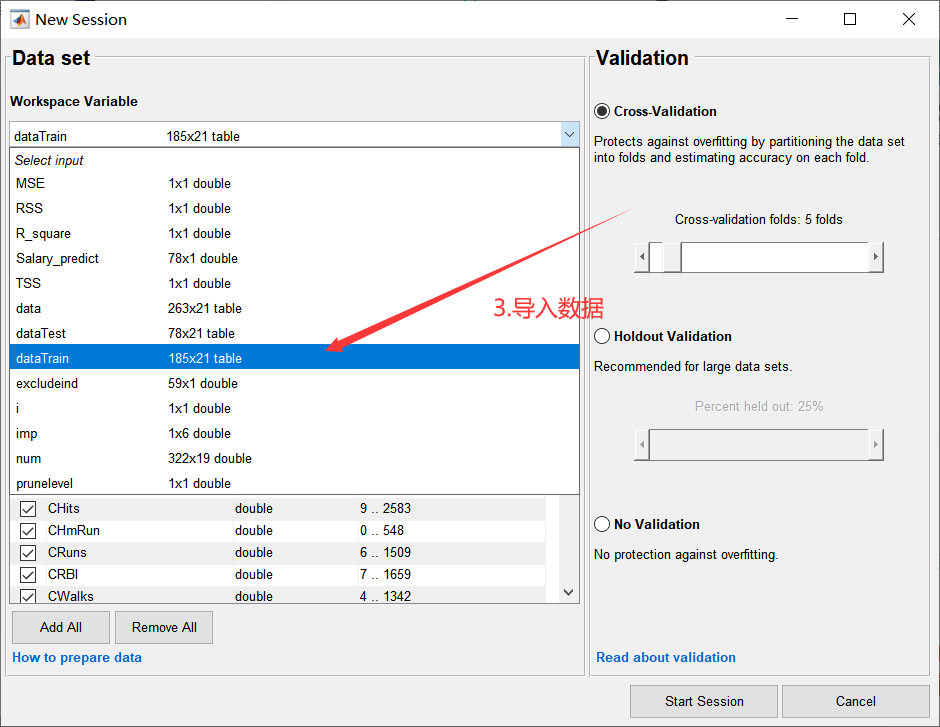

如下所示,也可以贪心一点,全部都选,选择All

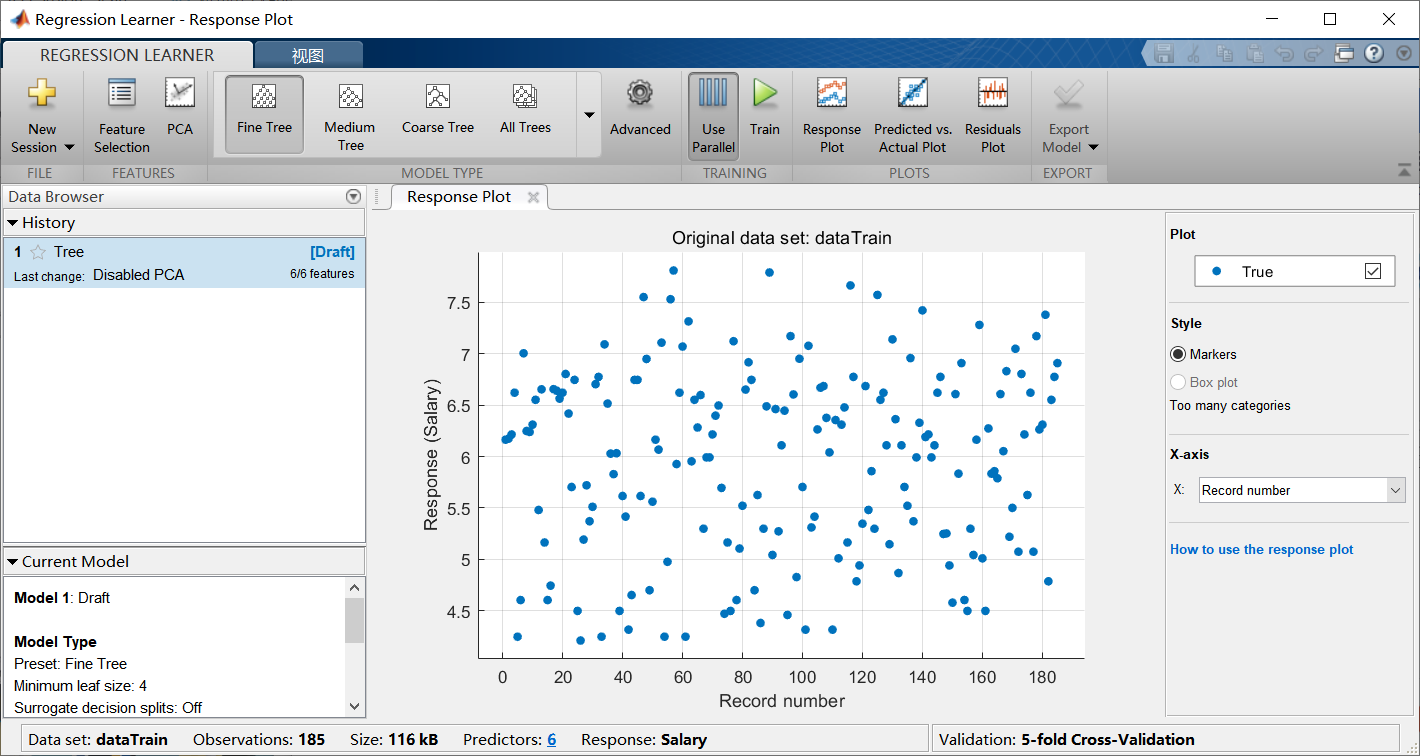

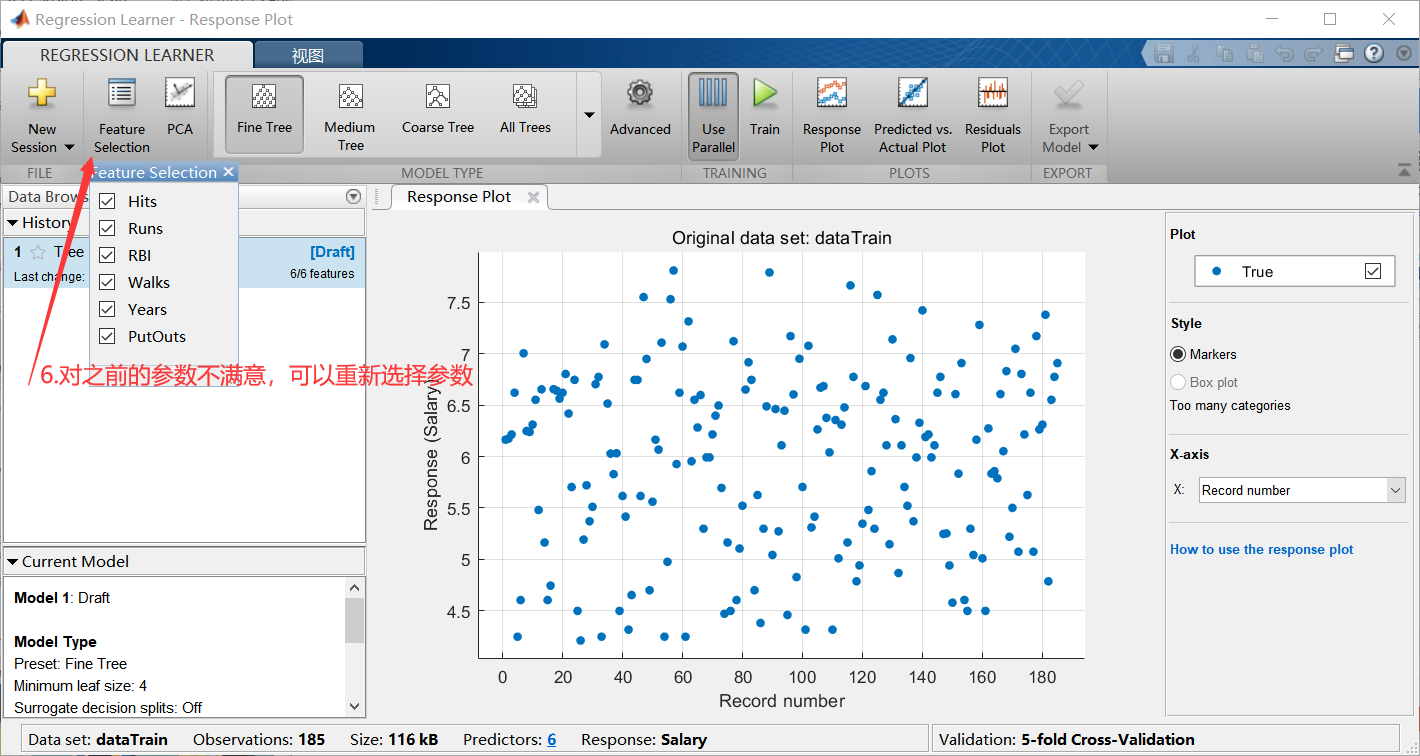

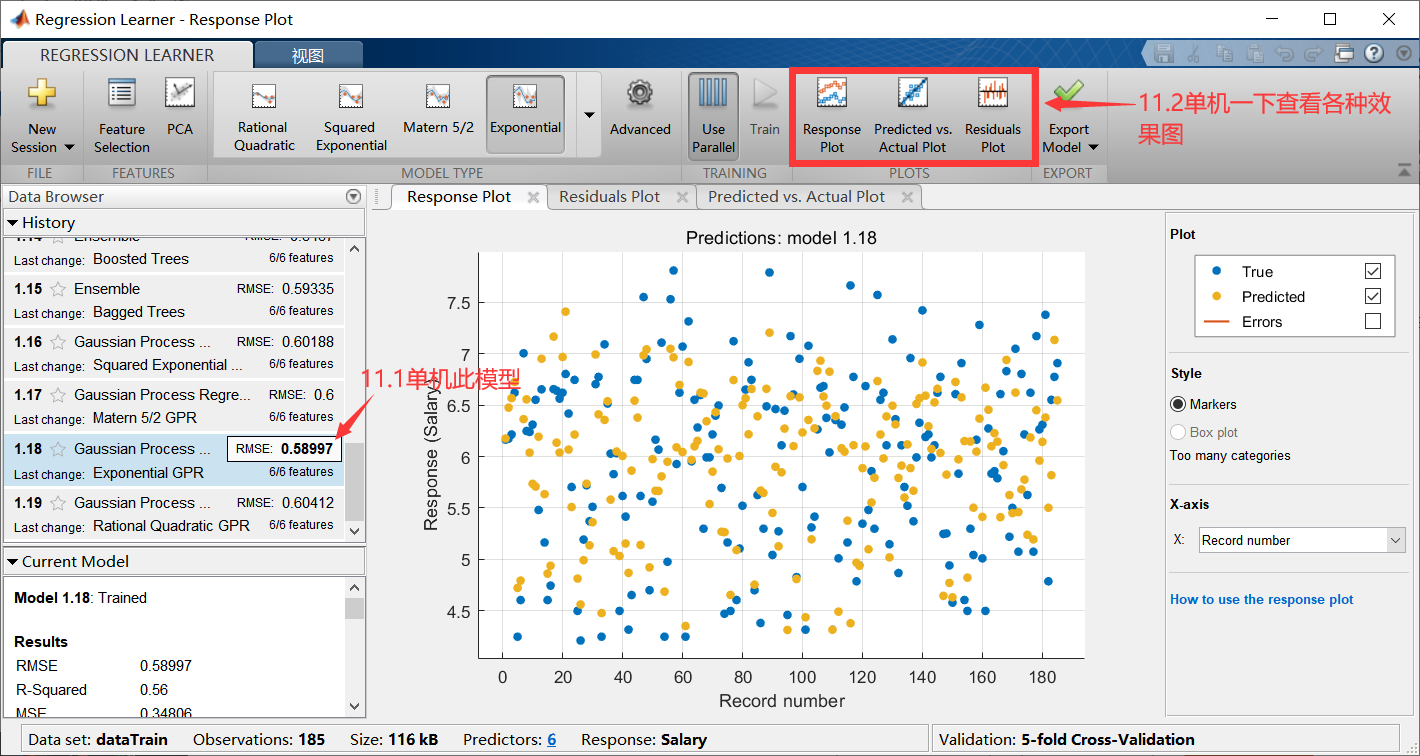

单机任意一个模型之后,可以查看各种效果图:

Original: https://blog.csdn.net/pxyp123/article/details/123425987

Author: pxyp123

Title: 第五课:回归分析

原创文章受到原创版权保护。转载请注明出处:https://www.johngo689.com/630361/

转载文章受原作者版权保护。转载请注明原作者出处!